Sno Falls CU takes on startups with robo-adviser

Sno Falls Credit Union, which has 6,500 members, is launching a robo-adviser to boost its wealth management business and keep members away from the likes of Betterment and Wealthfront.

“Betterment now offers checking accounts,” said Tim Williams, president and CEO of Sno Falls Credit Union. “Once our members go over to Betterment, they are going to be marketed checking accounts, so we might lose that relationship.”

The Snoqualmie, Wash.-based credit union is using technology from Access Softek, a digital banking software vendor, to launch the robo-adviser, which Sno Falls is branding as “Sno Falls Smart Invest.” The credit union is the first client to offer Softek’s new EasyVest robo-adviser platform, which the company took live last week.

Automated investing is an increasingly crowded field. Citizens Bank offers a robo-adviser, and Betterment and Wealthfront are both becoming more bank-like. Betterment also offers checking and savings accounts, and debit cards, while Wealthfront offers a savings account and plans to launch debit cards and direct deposits in the future. Vise, meanwhile, landed a $14.5 million Series A last week led by Sequoia Capital to continue helping advisers instantly create personalized portfolios.

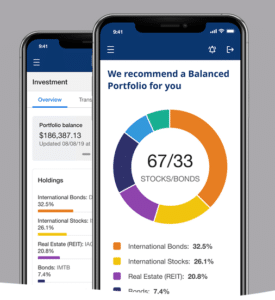

EasyVest runs on an algorithm that analyzes members’ time frame, risk appetite, income and goals to choose the right portfolio. According to Softek, only 2% of consumers interact with the wealth management programs offered by their banks or credit unions, and the EasyVest platform is designed to increase engagement. “Wealthfront and Betterment pioneered the robo-adviser model years ago, but what is new here is the seamless integration with online and mobile banking, and having the service brought to you by your credit union,” said Chris Doner, CEO of Access Softek.

See also: Citizens arms robo-adviser with cash account

Doner said the San Francisco-based company spent about two years developing EasyVest. Before the full launch, Sno Falls had been beta testing the robo-adviser for the past few months with its employees, according to Williams. The pricing for EasyVest varies on a case-by-case basis and depends on what costs are charged to the end user. Softek has four other clients implementing EasyVest, according to Doner. While all those clients are credit unions so far, the company said the tool can also help banks.

In addition to EasyVest, Softek offers solutions for mobile banking, account opening, lending and video chats. According to Williams, Sno Falls was drawn to EasyVest because the credit union could integrate the robo-adviser directly into its app and online banking channels.

“We need to control the relationship with our members,” Williams said. “When Access Softek approached us with their idea for a robo-adviser, we were really excited. Members are on our ecosystem and our online banking platform, so we can offer all those robust products in one place.”