Tech Focus: Do chatbots have a long-term future after COVID-19 bump?

For Advia Credit Union, digital chatbot technology from LogMeIn was a “saving grace” according to Joli Hensley, manager of digital channels. The chatbots, which answered basic questions about COVID-19 relief and online banking, helped credit union employees focus on more complex questions and kept the credit union from outsourcing customer service calls to a third party.

“You take something like COVID, which is doubling our call volume — and you can just imagine what that could have been, as far as a further economic hurt for us to have all that overflow — that we’re now able to keep in-house and deflect with the technology,” Hensley said during a virtual webinar earlier this month hosted by LogMeIn, a software provider headquartered in Boston.

Advia’s story represents a larger trend. Chatbot technology companies have seen a spike in volume from their clients since the start of the COVID-19 pandemic. San Mateo, Calif.-based Interface, for example, saw a 140% jump in use by existing customers, according to founder and CEO Srinivas Njay. Chatbot companies believe the spike signals a shift in banks’ priorities, but time will tell if a COVID-19 bump will translate to long-term adoption.

Seizing the moment

Interface’s conversational AI technology powers automated call centers and digital chatbots for clients, which include State Bank of India, a Mumbai-based bank with more than $550 billion in assets, as well as Texas Dow Employees Credit Union and Security Service Federal Credit Union. Interface’s value proposition is the promise to clients that it can automate 60% of call center queries within 60 days, and any answer the platform doesn’t know can be added within 24 hours. Its technology even helped lenders walk small business customers through Paycheck Protection Program loan applications, a notoriously confusing process that befuddled bankers and borrowers alike.

While customers avoid branches despite financial uncertainty resulting from the COVID-19 pandemic, banks are finding new ways to reach them. According to Njay, banks and credit unions are seeing a 40%-50% increase in call center volume since the start of the pandemic. With clients doubling down on their chatbot bandwidth, Interface has seen a 300% increase in revenue from existing clients, he said.

The COVID-19 spike isn’t a flash in the pan, according to Njay, adding that the swell in volume will jumpstart long-term adoption of chatbot technology for both institutions and consumers. Consumers who have been slow to use chatbots, namely Gen Xers and Baby Boomers, are now being forced to use the technology, and a positive experience will turn them into long-term users, he said. In fact, consumers are three times as likely to use a chatbot after they have initially tried it, according to data from Interface.

“[Chat] is already becoming a significant channel that financial services are investing in,” Njay said. “Every financial institution is pushing hard on self-servicing,” and there is potential for growth. Only 30% of transactions are recurring, meaning the remaining 70% is ripe for some form of assistance or self-service, according to Interface.

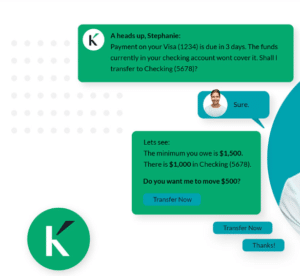

In addition to encouraging consumers to self-serve quick questions during the pandemic, chatbots have helped banks and credit unions alleviate mounting call center volume. The technology goes beyond helping bank customers, as employees can also benefit from chatbots that disseminate information while they work from home away from their senior leaders, said Tiffani Montez, a senior analyst with Aite Group’s retail banking practice.

For one, Corning Credit Union stood up an internal chatbot powered by LogMeIn in five days to disseminate accurate and up-to-date information to frontline employees, who were struggling to navigate the complexities of government stimulus and relief packages while working remotely. The bot was a necessary upgrade from the internal chatroom previously used by call center employees, according to Chad Hessler, the credit union’s supervisor of digital services and support. Corning, which serves 112,000 members in New York, North Carolina and Pennsylvania, had logged more than 2,000 interactions with the bot in the first month, with the technology answering about 80% of questions.

Putting brain behind the bots

Whether lenders will see success with chatbots beyond COVID-19, however, depends on their resolve to grow the platform, according to Montez. “The key point to keeping that adoption is continuing to evolve the experience,” she said. “If [lenders] go stagnant and just create COVID use cases and don’t iterate, then it won’t happen.”

New York-based Kasisto, another conversational AI company that works with the likes of JPMorgan Chase, TD Bank and Standard Chartered, has seen a 35% increase in volume on its platform between February and April, according to Chief Marketing Officer Stephen Epstein. The company was spun out of Stanford Research, the same group that built Siri, according to Epstein. For the first time in his experience, banks are treating digital channels as part of their disaster-recovery process, he said, and the pandemic has opened banks’ eyes — and wallets — to digital chatbots.

To ensure long-term success beyond a pandemic spike in volume, Epstein said Kasisto is diving deeper into data analysis for its AI platform, KAI. Since the start of the pandemic, the company has hired a full-time employee solely dedicated to data analysis and working closely alongside the product team so that the insights from the data consistently influence product design.

“When we see unknown questions, we are categorizing and clustering them. We’re understanding the importance of them. We’re building new responses into KAI so KAI can answer these questions more holistically,” Epstein said. “We’ve always done that, but what COVID taught us was to do it more often and more diligently.”

By diving deeper into analytics, Kasisto has been able to categorize the various types of consumers who interact with the platform. There are what Epstein called the “Questioner,” or the type of consumer who asks multiple questions and follow-ups to any response; the “Inquirer,” who just wants to get the information and move on; and the “Learner” who uses the platform to gain financial knowledge.

See also: Banks retool customer service in the scramble for PPP loans

Despite the chatbot boom, the challenge to keeping the momentum will be overlaying the experience with data that can help consumers, according to Aite’s Montez. Simply providing answers to consumers’ questions isn’t as valuable as providing a chatbot that gives advice they can act on within banks’ digital channels. “[Banks] need data and analytics for consumers on how their actions affect their financial health,” Montez said. “How do you create experiences for consumers that allow them to achieve peace of mind that help them meet their financial goals?”

Kasisto and Interface both said they are continually funneling new data into their AI platforms and teaching them new insights, too.

“We only focus on financial services, and we already process millions of conversations across customers and members of financial institutions worldwide every single day,” Interface’s Njay said. “That kind of volume helps us continue to build this machine learning model that is available Day One.”