Looking to beat Apple to the punch, digital competitors roll out cashback cards

The jury is still out whether the Apple Card will be the disruptive force that Apple has claimed it will be. Fintech firms and banks, in the meantime, appear eager to roll out some cash back card products of their own.

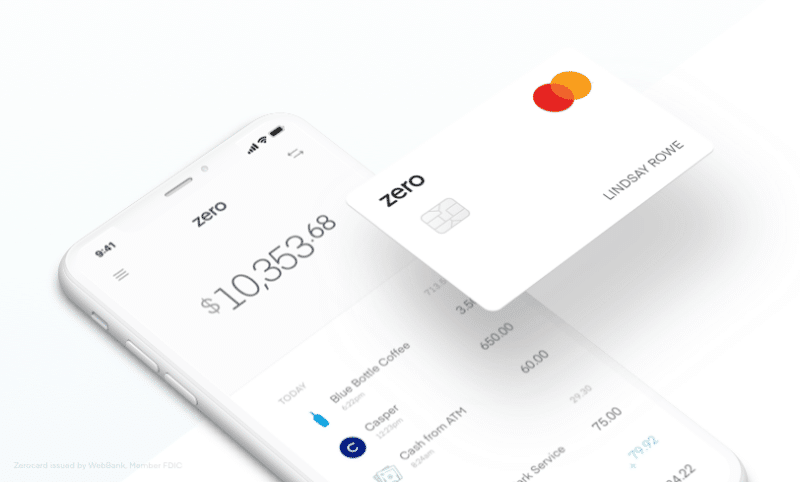

Tuesday’s launch of Zerocard, a “debit-style” credit card from fintech firm Zero, in partnership with WebBank, Evolve Bank & Trust and Mastercard, coincided with a debit card and bank account offering from Green Dot and Visa. Both products come with an accompanying mobile banking app. Additionally, both are low on fees and high on rewards, offering up to 3% cash back on purchases — with different caveats.

While both are rolling out ahead of the anticipated August launch of Apple Card, a virtual credit card that Apple developed in partnership with Goldman Sachs and Mastercard, it’s worth noting that Green Dot powers Apple Pay Cash services that allow users to receive, send or spend funds through their Apple Pay accounts. Nonetheless, the model of a payment card with a dedicated mobile app that allows users to track transactions and rewards is becoming a familiar one in the industry.

Thad Peterson, senior analyst at Aite Group, said that, while Apple Card will have a commanding lead in terms of user experience and functionality, its Achilles heel is that Apple Pay adoption and usage is still low, opening a door for traditional credit and debit card products. He believes both companies are trying to get out in front of Apple Card and expects more “copycats,” particularly in terms of user experience, in the coming months.

“I think what they’re also trying to do is, to some extent, emulate what Apple potentially is offering, particularly with the information flow,” Peterson said. “On the cashback side of things, the challenge that they face versus the Apple Card is that it’s essentially native to the app. It’s not something that you have to add on; it’s just there. That’s going to be a really difficult thing for them to overcome.”

Jennifer Bailey, vice president of Apple Pay, has said Apple Card users will be able to sign up for the card from their iPhone and begin using it in minutes. Users also can keep track of weekly or monthly spending, minimum payments due and transaction history, which she added will be untangled and cleaned up through the use of Apple Maps and machine learning.

Zerocard is a rewards credit card, issued by Salt Lake City-based WebBank, paired with an FDIC-insured checking account, called Zero Checking and powered by West Memphis, Ark.-based Evolve Bank & Trust.

Bryce Galen, founder and CEO of San Francisco-based Zero, said whereas Apple announced a credit card that encourages customers to pay “less interest,” Zero has done one better by launching what he claims to be the first credit card that encourages customers to pay “no interest.” He noted that cash back of up to 3%, rewards of up to 2% on net deposits and no fees, as well as instant money transfers and rewards redemptions, make Zero “stack up favorably against any competitor offering.”

Although Zerocard offers customers the option to revolve, as with a traditional credit card, Galen said 90% of the app’s existing users (part of a limited beta test) have chosen to use the Debit-style Experience function, in which the limit on their card is informed by deposits made into their Zero Checking account. The balance is automatically paid at the end of each billing cycle. In practice, however, the product is similar to a secured credit card with cashback rewards, much like the product Amazon launched in June.

Activating the Debit-style Experience means that users won’t overspend, Galen claimed, because transactions are approved only up to the customer’s current position, meaning their Zero checking account balance minus Zerocard balance. If turned off, transactions in excess of the customer’s Zero Checking balance can be approved, and customers can pay their statement each month either manually or automatically from Zero Checking or from another bank account.

In terms of the features available through the app, Galen touted transaction history that includes the full name of the merchant, logos, maps, hours and contact info from data sources like Google and delivered instantly via push notification. The app also allows for instantaneous funds transfers and rewards redemptions with the swipe of a finger, he noted.

Zerocard offers up to 3% cash back on qualified purchases and is available in four levels – Quartz, Graphite, Magnesium and Carbon – with a corresponding increase in the percentage of cashback earned. Levels of cards are granted based on annual spending and/or customer referrals.

Also on Tuesday, Pasadena, Calif.-based Green Dot launched its Unlimited Cash Back bank account with connected Visa debit card and mobile app. Green Dot said it is not trying to compete with Apple, adding that the Apple Card is a credit card product as opposed to Green Dot’s bank account and debit card product. The company emphasized what it called a savings crisis in the U.S., pointing to a Federal Reserve Board report that found four in 10 Americans do not have adequate savings to cover an unexpected expense of just $400.

Green Dot’s offering includes unlimited 3% cash back on online or in-app purchases and an FDIC-insured high-yield savings account with 3% annual interest on deposits up to $10,000. The company also touted no overdraft fees and no bounced check fees, no minimum balance requirements and no monthly fee (when the customer spends $1,000 or more using the card), access to free ATMs and the ability to make free cash deposits at participating retailers. The app offers mobile check deposit, a peer-to-peer payments service, free electronic bill pay and a “fun and intuitive” design allowing customers to track spending, savings and the amount earned in cashback bonus money.

Asked if Green Dot could run into competition with Apple Card with the offering, Michael Keeslar, general manager of consumer products at Green Dot, did not think so. “We’ve created a debit card product that we believe can compete in the credit card space,” he said. “We also wanted to expand the addressable market to those with whom our prepaid products may not have resonated in the past.”

This story was updated at 10 a.m. ET, July 31, with additional comments from Green Dot.