BAS 2020: Wealthfront eyes faster money movement, integrations for Autopilot

Wealthfront is refreshing its Autopilot product, as the digital fintech looks towards faster funding and a larger catalog of destinations.

The Palo Alto, Calif.-based digital investing fintech is looking to provide same-day money movement for transactions and investments, and add more investing destinations in the next year. Founded in 2008, Wealthfront has 400,000 customers and has raised $204.5 million to date, according to Crunchbase. The company held $20 billion of assets under management as of September 2019.

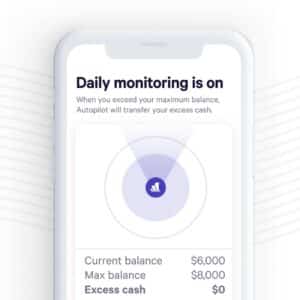

Autopilot, which launched in September, is designed to function as a financial assistant. Consumers predetermine how much money they need in a given Wealthfront account and the software automatically transfers excess cash into other investment or savings accounts, depending on the consumer’s goals.

Within 48 hours of launching, Autopilot automatically invested more than $3 million from client accounts, according to Head of Financial Automation Chris Hutchins, who spoke at the Bank Innovation Banking Automation Summit last week.

The idea is to integrate a system that works on all fronts for the consumer, automatically distributing funds to pay bills as well as top off savings and retirement accounts. Recent trends around security, privacy and fraud have prompted consumers to “put all their accounts in fewer places,” Hutchins said, a practice that is driving Wealthfront’s strategy.

Speed is another aspect of its platform that Wealthfront is tackling this year, Hutchins said. Currently, it takes multiple days for clients to initiate a transfer and invest the fund in the market; Wealthfront is building the capacity for that process to take place in the same day.

However, as Wealthfront looks to add new investing destinations and ramp up connectivity with bank accounts held at third-party institutions, it will need to wrangle slow integration technology. “That’s probably one of the biggest holes in the whole experience,” Hutchins said, “to the extent a client is required to hold an account at an institution that doesn’t have APIs.”

The ability to balance different accounts against one another, so that a customer can automate saving and investing between accounts and debts, is another project slated to launch during the next year, he said.

Click here to read more news from Banking Automation Summit

The enhancement plans come as the fintech continues to bulk up its offerings. Before launching Autopilot in September, Wealthfront added checking account features, like debit cards and bill payment, to its cash accounts in June. Wealthfront partners with $2.59 billion dollar Green Dot Bank, a Pasadena, Calif.-based subsidiary of Bonneville Bank, to offer the checking products to its consumers.

Despite an increased interest in synchronized accounts, some consumers may still need convincing to transfer their finances into such a new system, according to Sophie Schmitt, a senior analyst on Aite Group’s wealth management team.

“There’s certainly still value in speaking with an advisor, and it’s going to take time to change behaviors,” Schmitt explained, noting individuals from the Generation-X and baby boomer generations already have established relationships with traditional advisors.

“I think they’re providing a huge value, especially for young people,” Schmitt said of digital fintechs. “They’re not just offering products, but they’re offering these algorithms with the services on top.”