Wells Fargo to Take New App National by Year’s End

As the mobile-first generation starts to earn more money, the arms race to earn market share is heating up as large banks look to grow their digital-only brands and earn lifelong customers. Indeed, Wells Fargo is stepping up its digital-only banking game with a plan to launch its Greenhouse app nationwide by the end of the year.

Challenger banks like Chime, N26 and Revolut are completely digital, while JPMorgan Chase launched its Finn platform nationwide in June 2018. So, when it comes to setting its app apart from the growing number of digital banking options, Well Fargo hopes that Greenhouse, which is separate from the normal Wells Fargo app, can be more forward-looking.

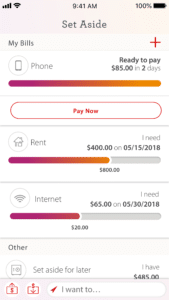

According to Peggy Mangot, senior vice president of innovation at Wells Fargo and the head of Greenhouse development, the new digital-only platform allows customers to split their money into an account for bills and an account for spending that is linked to a debit card. With some input from the customer, Greenhouse even can prompt customers to put away the right amount into the bills account as soon as money is deposited.

“As an industry, we do a fairly good job of saying, ‘This is how you spent your money’,” Mangot said in an interview with Bank Innovation. “That’s very much of a look back. What Greenhouse does that is very different and unique is it’s proactive.”

How it works is users tell the app what bills they have to pay regularly, and Greenhouse prompts them to put enough money into the bills account. The remaining amount goes into spending so users can see exactly what they have left to spend on expenses that aren’t bills.

Mangot said this system helps customers stay on top of their finances better than simply showing how they spent their money in past months. Other banks have similar features, such as the digital-only bank Simple with its Safe-to-Spend feature that calculates how much spending money you have after you subtract upcoming bills. Wells Fargo, however, believes that prompting users to split up their money into separate categories and linking only spending to the debit card will keep them more on track.

Mangot couldn’t say what specific tweaks Wells Fargo has made to Greenhouse during the pilot, which launched in California, Oregon, Washington, Texas, Pennsylvania, Florida and New York in November, but she said the ability to separate money into two categories has been popular. During the research phase, Wells Fargo found people were using anything from spreadsheets to calendar apps to physical envelopes to keep track of bills.

Greenhouse is just one example of banks fighting for a market share of millennials and Generation Z. “A sub-brand can be an effective strategy for client acquisition,” April Rudin, founder and CEO of the financial services marketing firm The Rudin Group, said in a message to Bank Innovation. “These large banks are using a sub-brand to attract millennials who may be turned off by big brand banking.” Indeed, she pointed to the barrage of negative press that Wells Fargo has received in recent years.

Mangot won’t call Greenhouse an app for one particular group. Rather than targeting millennials or gig economy workers, Wells Fargo uses the term “new to banking” to describe the demographic. “It’s intentionally a big tent,” she said. “When you think about money management and the struggles that people have, it is across the typical target segments.” Conveniently, this definition also allows Wells Fargo to target more people, although she declined to specify how many people have signed up so far.

Newer, standalone banking apps might provide insight that can benefit the bank’s core products. “The usage metrics and engagement on these apps can be compared to the traditional technology, products and services the bank offers,” said Lane Martin, partner and lead of the U.S. banking domain at the financial services consulting firm Capco, in an email to Bank Innovation. “Catering to sub-segments and being able to compare performance helps banks build better products in the future.”

Mangot is happy the bank made Greenhouse a standalone app so her team could experiment without interrupting normal operations for the majority of Wells Fargo customers. She said it’s too early to tell if the end goal is to fold Greenhouse into the traditional Wells Fargo app.

Greenhouse is only seven months old, and the app is still developing. “This is a tough nut to crack,” Mangot said. “Our focus is getting the basics right: helping [customers] with paying bills on time, controlling spending and starting to build savings.” However, given the rapidly changing nature of financial technology, Wells Fargo could have more updates to share in a year or even six months, she noted.