Ready, set, pay: Prepping for FedNow

Fed’s real-time payments rail to launch in July

The launch of FedNow is finally around the corner and it’s been a long time coming, industry experts told Bank Automation News.

The launch of FedNow is finally around the corner and it’s been a long time coming, industry experts told Bank Automation News.

“The launch reflects an important milestone in the journey to help financial institutions serve customer needs for instant payments to better support nearly every aspect of our economy,” Tom Barkin, president of the Federal Reserve Bank of Richmond and FedNow program executive sponsor, said in a Federal Reserve release.

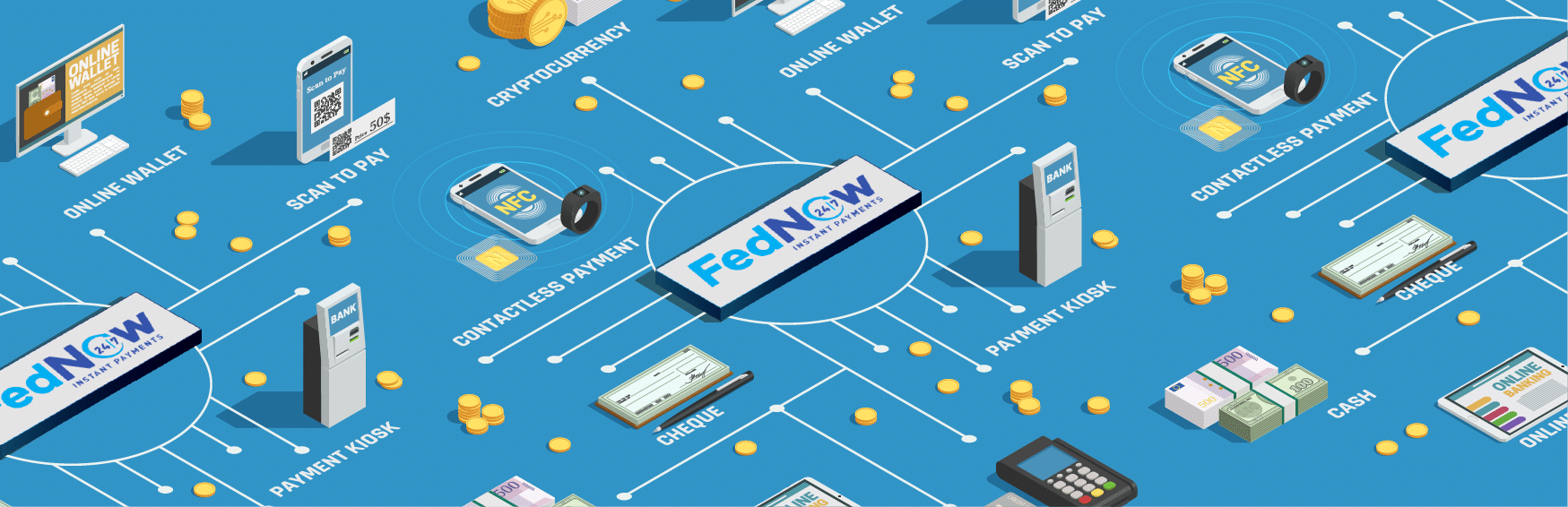

The Federal Reserve announced the real-time payments network in August 2019, and now that the system will go live in July, financial institutions and vendors alike are prepping their tech stacks for the new rail.

FedNow is expected to bring instant payment services to U.S. financial institutions around the clock, allowing for funds to hit accounts instantly, a function that is in high demand, according to the Fed’s website. In fact, the Fed reported that 70% of consumers want faster payment capabilities from their FIs.

For example, if you look at existing payment rails, “they are clunky,” Matt Tymn, chief revenue and marketing officer at FFB Bank, said last week at Fintech Nexus USA 2023 in New York. When a merchant, like a restaurant, wants to be paid over the weekend or after business hours, it doesn’t happen. With FedNow, “if you look at it as 365/24/7, it just changes the whole landscape of the way payments function.”

“With the launch drawing near, we urge financial institutions and their industry partners to move full-steam ahead with preparations to join the FedNow service,” Ken Montgomery, first vice president of the Federal Reserve Bank of Boston and FedNow program executive, said in a March Federal Reserve release.

Scott Young, vice president of payments operations for Hawaii USA Federal Credit Union, told BAN: “In order for a bank or credit union to get prepared for FedNow, in addition to having conversations with their service providers, they need to internally decide what their strategy is for instant payments. The sooner [FIs] start with these conversations, the better, because this is where the payments landscape is moving.”

‘Walk before you run’

As financial institutions of all sizes prep for FedNow, they must consider how they will use the platform, who their tech provider will be, what technology needs to be updated and what personnel needs to be in place, Tede Forman, president of Jack Henry payment solutions, told BAN. “We recommend a ‘walk before you run’ process for institutions new to the network.”

Ahead of transitioning to FedNow Forman and other experts say FIs should consider the following:

Step 1: Vendor selection

Financial institutions must, first and foremost, have conversations with vendors and service providers to determine what the FIs need to prepare for the launch of FedNow, HawaiiUSA FCU’s Young said.

“Being a small financial institution in the middle of the Pacific, we needed to partner with our service providers,” he said. “Since FedNow will be a 24/7/365 payment rail, financial institutions will need to heavily rely on automation from systems that are equipped to handle such transactions.”

Service providers for the payments rail include Finastra, Fiserv, FIS and Jack Henry, according to the Fed website. HawaiiUSA is using Jack Henry’s solution, Young said.

Fiserv, for one, offers two solutions to connect to the federal network: NOW Gateway and Payments Exchange, Parag Rohan Jain, general manager for real-time payments at Fiserv, told BAN.

Step 2: Evaluating use cases

Banks must decide how they will use FedNow: to send payments, receive payments or both, Forman said, noting that FIs should consider “beginning in a receive-only mode before adding send use cases.”

Gartner Analyst Debbie Buckland reiterated this, saying: “If you’re a little nervous about delving in, just receiving is quite fine just to set up the pipe.”

Banks will be able to add functionality after the pipeline is in place, she added.

Step 3: Staffing and training

As FedNow hits the market, banks should ensure their teams are trained on the network, Forman said. “Consider sending staff to train on the new networks, talk to your vendors and get educated.

“Read the materials shared by the network and identify where you have gaps,” he added, noting that Fed reps and core providers can assist in training. The FedNow website also has a readiness assessment.

Step 4: Risk mitigation

Risk and compliance teams must be deployed when implementing FedNow, Forman said.

“From a fraud-mitigation perspective, they will need to be able to gather enough information at the point the consumer reaches out to them to be able to bucket fraud and scams,” he said, referring to a bank’s ability to categorize fraud quickly.

Banks must look at their fraud-detection capabilities to learn whether updates are necessary, Gartner’s Buckland said. Make sure the fraud solutions that are in place “can handle the real time nature of these transactions, because now that these transactions are getting initiated and settled quicker, you need to be able to call out what you believe to be a fraudulent transaction in real time as well,” she recommended.

Step 5: Customer education

Just as bank systems must be able to mitigate fraud, customers, too, must be educated to watch for scams, phishing attempts and red flags, Buckland said.

Early adopters

FedNow’s pilot program, which includes more than 110 organizations, supports the development, testing and adoption of FedNow, according to the FedNow website. Pilot program participants include U.S. Bank, Wells Fargo Bank, Michigan State University Federal Credit Union, Regions Bank and Cross River Bank, among others, according to the Federal Reserve’s website.

Another participant in the pilot is New England-based Salem Five, the $6.6 billion bank’s Head of Digital Delivery Rob Ames told BAN. The bank is using Fiserv’s solutions to pilot the payment rail.

“In terms of preparing the organization and deciding to be an early adopter, part of that was within our DNA,” Ames said. “We, as a company, have typically been attracted to adopting technologies earlier than others.”

The bank, Fiserv and the Fed worked together throughout the pilot so that when the time to launch comes, the bank can be “in production with the Fed on Day One,” Ames said.

Fiserv has six banks in the pilot phase, Chief Executive Frank Bisignano said during the tech provider’s Q1 2023 earnings call, noting that 20 financial institutions are committed to go live with FedNow when it launches in July.

“If you’re looking at [FedNow], and you’re curious about it, there’s a world of opportunity for you,” FFB Bank’s Tymn said. “FedNow is going to open up a whole new world for smaller community banks.”