Loan process automation fintech Blend headed for IPO

US Bank, BMO Harris credit Blend with reductions in their loan cycles

Banking process automation fintech Blend Labs experienced 90% year-over-year revenue growth to $96.0 million in 2020 from $50.7 million in 2019, while losses decreased, the company’s Monday S-1 filing revealed. The filing comes ahead of Blend’s proposed public listing on the New York Stock Exchange with the ticker symbol BLND.

During the same period, the company reported a net loss of $74.6 million for 2020, down from $81.5 million in 2019, the filing revealed. The company plans to issue both Class A and Class B stock, according to the filing, with Class B stocks going to the co-founder and head of Blend, Nima Ghamsari. A projected per-share price was not listed in the filing. Class A stocks will offer one vote per share, whereas Class B will have 40 votes per share.

Blend is a white-label software-as-a-service company founded in 2012 that automates and digitalizes aspects of the lending process for mortgages, personal and auto loans, and automates credit card and deposit account applications. In March, it acquired Title365, an escrow and settlement company, for $500 million with plans to integrate those services into its platform.

The company’s 291 customers include 31 of the top financial services firms in the U.S., by total assets managed. Wells Fargo, U.S. Bank, M&T Bank, Truist, BMO Harris Bank, Elements Financial Federal Credit Union and Mountain American Credit Union were specifically mentioned in the 205-plus page filing, which reveals how financial institutions have deployed Blend to decrease loan cycles.

The $550 billion U.S. Bank credited Blend with cutting mortgage loan cycles by 10 days on average and reducing home equity loan cycles from 40 days to 21 days. The $973 billion BMO Harris Bank saved over 100,000 hours of processing time for home equity applications in a year, and increased digital home equity applications by 253% year-over-year from 2018 to 2019, according to the filing. Elements Financial Federal Credit Union, with $2 billion in assets, reported an 11% average increase in approved applications and a 60% reduction in submission times for vehicle loans, personal loans and credit cards using Blend.

Blend uses open APIs to integrate into the back-office systems of financial institutions, as well as to connect with partner technology, data and service providers.

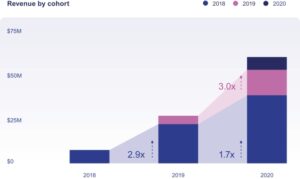

“Once deployed, we become deeply embedded in business processes and integrated with back-office systems, which makes us difficult to replace,” Blend stated in the filing. “This gives us a strong vantage point to be able to cross-sell additional offerings to our customers.” To back up that assertion, the company incorporated a graph showing that most of its growth during the past three years has come from existing, rather than new, clients.

It’s worth noting, however, that among its risk factors, Blend specifically noted that “a large percentage of our revenue is concentrated with a small number of key customers,” with 18 customers generating more than 53% of the company’s 2020 revenue. Other risk factors mentioned are the company’s history of net losses and market competition from internal builds at financial institutions.

Blend’s ecosystem includes more than 45 technology partners, 29 data partners, 1,200 marketplace partners and more than 900 settlement services partners. The data partners, which help automate verification checks and reduce the need for consumers to upload documents, include credit bureaus, payroll service providers, tax preparers and anti-fraud services. The filing did not disclose specific tech partners, but noted that its technology vendors include integrations with “leading providers of CRM platforms, loan origination systems, core banking systems, document generation systems, and pricing and product engines.”

So far, Blend has raised a total of $665 million over nine funding rounds, with the latest being a series G round in January, according to Crunchbase. Goldman Sachs, Allen & Company, and Wells Fargo Securities are underwriting the proposed offering.